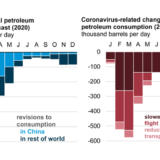

IEA projects global oil demand to contract by 435 kb/d in Q1 due to Covid-19

Global oil demand has been hit hard by the novel coronavirus (Covid-19) and the widespread shutdown of China’s economy. Demand is now expected to fall by 435 thousand barrels per day (kb/d) year-on-year (y-o-y) in the first quarter of 2020, the first quarterly contraction in more than 10 years, according to the International Energy Agency (IEA).

The IEA’s latest Oil Market Report (OMR) has reduced its 2020 growth forecast by 365 kb/d to 825 kb/d, the lowest since 2011. Lower-than-expected consumption in the OECD trimmed 2019 growth to 885 kb/d.

The impact of the novel coronavirus, which is a major global public health emergency, is still unfolding globally. There is already a major slowdown in oil consumption and the wider economy in China. While the SARS epidemic of 2003 is widely used as a reference point for analysis of Covid-19, China has changed enormously since then. Today, it is central to global supply chains and there has been an enormous increase in travel to and from the country, thus heightening the risk of the virus spreading. In 2003, China’s oil demand was 5.7 million barrels per day (mb/d) and by 2019 it had more than doubled to 13.7 mb/d (14% of the global total). Moreover, last year China accounted for more than three-quarters of global oil demand growth.

The coronavirus outbreak has also led the IEA to revise down the outlook for global refinery runs. Chinese crude throughputs for the first quarter have been cut by 1.1 mb/d and are now expected to contract by 0.5 mb/d year-on-year. As a result, global runs are forecast to expand by just 0.7 mb/d in 2020. The launch of IMO’s new bunker fuel regulations in January boosted simple refining margins based on sweet crudes.

The impact of Covid-19 for oil prices have been sharp: Brent values fell by about USD10/barrel (bbl), or 20%, to below USD55/bbl. Before Covid-19 came along, the market was already nervous in anticipation of a supply overhang of 1 mb/d in the first half of 2020 due to continued expansion in the U.S., Brazil, Canada, and Norway. Even threats to security of supply, e.g. tension in Iraq, a 1 mb/d fall in Libyan oil production, and force majeure declared for some Nigerian cargoes, had little impact on prices. Now that the demand outlook has weakened, prices have moved significantly down.

From the point of view of the producers, before the Covid-19 crisis the market was expected to move towards balance in the second half of 2020 due to a combination of the production cuts implemented at the start of the year, stronger demand and a tailing off of non-OPEC supply growth. Now, the risk posed by the Covid-19 crisis has prompted the OPEC+ countries to consider an additional cut to oil production of 0.6 mb/d as an emergency measure on top of the 1.7 mb/d already pledged. Lower oil prices, if sustained, are also bad news for highly responsive U.S. oil companies, though the IEA believes that we are unlikely to see an impact on output growth until later in the year. The effect of the Covid-19 crisis on the wider economy means that it will be difficult for consumers to feel the benefit of lower oil prices.