Cation Capital Files Proxy Circular and Releases Letter to Crescent Point Energy Shareholders

Urges shareholders to vote their BLUE proxy or BLUE VIF in favour of

four highly qualified independent nominees

Warns shareholders not to be fooled by the Company’s self-interested

attempts to distract from the real issues

Since 2013 shareholders have paid $93.5 million to named executives

only to lose $10.7 billion of equity value

CALGARY, Alberta–(BUSINESS WIRE)–Cation Capital Inc. (together with its affiliates and associates,

“Cation Capital” or “Cation”), a private investment firm, today

announced that it has filed its proxy circular and letter to

shareholders of Crescent Point Energy Corp (TSX/NYSE: CPG) (“Crescent

Point” or “Company”) to be mailed in connection with the Company’s 2018

Annual General Meeting of Shareholders to be held on May 4, 2018.

Shareholders of record as of March 22, 2018, are entitled to vote at

this meeting.

At the meeting, Crescent Point shareholders will be asked to vote “FOR”

fixing the number of directors to be elected at the Meeting at ten; “FOR”

the election of the Cation Nominees: Dallas J. Howe, Herbert C. Pinder,

Thomas A. Budd and Sandy L. Edmonstone and “AGAINST” the approval

of an advisory resolution accepting the Company’s approach to executive

compensation.

Sandy L. Edmonstone, President of Cation Capital, said, “In our view,

shareholders of Crescent Point Energy have been abandoned by the current

Board and management. This sentiment is all too clear in the Company’s

decision to attack a shareholder of record and turn a proper nomination

process, one imposed by the Company itself, into some sort of nefarious

fiction. Rather than defend their track record, which is impossible

given the billions of equity value lost over the last five years, the

Company has resorted to insulting some of the most experienced and

respected professionals in Canada. They have debased themselves much as

they have debased the Crescent Point stock.”

Added Edmonstone, “Cation’s nomination of four highly skilled,

experienced and independent director nominees represents an opportunity

for all shareholders to vote for needed change, change that will bring

about rigor, performance and a change in culture at Crescent Point. Our

four nominees are aligned with shareholders, owning over double the

number of shares than nine current non-employee directors combined.

Shares that were bought, not awarded, on the basis that the assets of

Crescent Point present an attractive investment opportunity. With better

leadership and the implementation of a plan to review operations,

capital allocation priorities and bring in accepted practices regarding

governance and compensation, we believe Crescent Point can begin a path

back to value creation. The company says it is making progress, how is a

stock hovering at 15 years lows progress? We urge our fellow

shareholders to vote for all Cation’s nominees on the Blue proxy card.”

Shareholders are urged to read the circular and vote their BLUE proxy or

BLUE VIF by 5:00 p.m. (Calgary time) on Tuesday, May 1, 2018.

Shareholders with questions about voting their shares should call

Cation’s strategic shareholder advisor and proxy solicitor, D.F. King,

at 1-800-835-0437 toll- free in North America, or 1-201-806-7301 outside

of North America (collect calls accepted), or by e-mail at inquiries@dfking.com.

Shareholders are also encouraged to visit www.FixCPG.com

to learn more about how the right people and right plan can create

long-term value for all. A copy of Cation Capital’s information circular

is also available on Crescent Point Energy Corp’s SEDAR profile at www.sedar.com.

The full text of Cation’s letter to Crescent Point investors follows:

Dear Fellow Shareholder,

We believe Crescent Point Energy Corp. (“Crescent Point” or the

“Company”) has tremendous long-term potential and the ability to create

significant value for all shareholders. However, like our fellow

shareholders, we at Cation Capital Inc. (“Cation”) are disappointed and

frustrated by the disastrous performance of Crescent Point and the

precipitous erosion of shareholder value.

Crescent Point’s share price has fallen drastically. The stock, once a

market darling, now lags its peer group in virtually all relevant

metrics and the incumbent members of the Company’s board of directors

(the “Board”) are either unable or unwilling to address the very serious

issue confronting the Company.

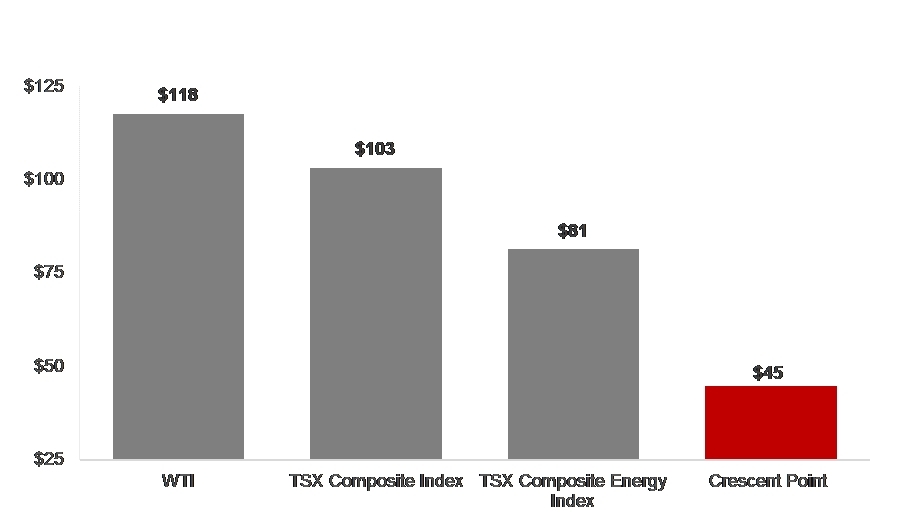

If you invested $100 at the beginning of 2015, your investment is now

worth… (See Chart 1)

| Note: | |

| (1) | Source: Bloomberg. |

The returns are worse if you have been a shareholder since 2013, all

the while management has been exceptionally well-compensated. (See

Chart 2)

| Note: | |

| (1) |

Market capitalization erosion calculated as market capitalization as at January 2, 2013 reduced by 76%. |

We believe Crescent Point’s dismal underperformance cannot be blamed on

external factors, as the Company is prone to do, but rather on flawed

strategy, poor execution, and ultimately failed governance by the Board.

Subsequent to Crescent Point’s surprise $650 million equity offering in

September 2016 at $19.30 per share, the Company’s shares have lost 52%

of their value, while relevant indices and other metrics have shown

growth or substantially smaller losses. The issue is clearly specific to

Crescent Point and it appears that the Board has been unable to

identify, let alone cure, what the exact problems are.

Simply stated, BILLIONS in shareholder

value has been destroyed

We believe the opportunity at Crescent Point is

unique, both in the amount of value that can be unlocked and how readily

it can be achieved. In an effort to unlock that value for

shareholders, Cation has nominated four highly experienced and

independent industry candidates – Dallas J. Howe, Herbert C. Pinder,

Thomas A. Budd and Sandy L. Edmonstone – for election to the ten person

Board at the Company’s upcoming annual general meeting, to be held on

May 4, 2018.

We have attempted to share our views and analyses with the special

committee established by the Board to deal with our proposal, with whom

we would prefer to work collaboratively. Despite our good faith efforts

to address our concerns outside of the public sphere, we continue to

receive no meaningful sign of collaborative engagement or that the

Company intends to address its numerous strategic and governance

challenges, let alone an external signal that the Company’s negative

trajectory has changed. Put simply, Crescent Point believes that its

current strategy is working! When the Company finally begrudgingly

met with us, all that they were prepared to offer is that they would

consider ONE of our nominees for a Board seat.

That will not do. Despite a rotation of six new directors since 2014

(with a seventh nominated this year) the Board has proven completely

ineffective at addressing any of the numerous issues facing Crescent

Point. The addition of one or two new directors will not suffice.

Crescent Point’s high board turnover coupled with its rigid adherence to

a failed strategy confirms what the street has known all along – that

Crescent Point is for all purposes controlled by and for a select group

of individuals. It is noteworthy that it is essentially this same group

– united by business interests outside of their service to Crescent

Point – that comprises the special committee of “independent” directors

that has rebuffed our attempts to effect necessary change at Crescent

Point. Crescent Point needs new leadership at the Board level involving

those with the expertise, vision and courage to stand in the face of the

entrenchment and cronyism that prevail today. A confident, independent

voice is needed.

Our nominees, whose compelling biographies are provided below, are

uniquely suited to this task and in preparation for this campaign have

invested substantial amounts of their own money to ensure alignment with

the all but forgotten shareholders of Crescent Point. As of the date of

the circular accompanying this letter, our nominees hold more than

double the amount of common shares held by all of the incumbent

non-employee directors.

Cation’s Nominees Bring Experience and a

Commitment to Restoring Shareholder Value

Cation’s nominees to the Board are:

-

Dallas J. Howe. Mr. Howe is the former Chair of the Board of

Potash Corporation of Saskatchewan Inc. He also is a former director

and Chair of the Compensation Committee of Viterra Inc., a Canadian

agribusiness built on the foundation of Saskatchewan Wheat Pool Inc.

and Agricore United. Mr. Howe has served on and chaired Corporate

Governance and Nominating, Audit and Compensation committees in the

private, public and not-for-profit sectors. Mr. Howe has been the

recipient of many achievements including, in 2009, being made an ICD

Fellow by the Institute of Corporate Directors. In his role as Chair

of Potash Corporation, Mr. Howe was instrumental in thwarting the

hostile bid initiated by BHP Billiton. In his position at Viterra, Mr.

Howe oversaw the acquisition of Viterra by Glencore International plc. -

Herbert C. Pinder. Mr. Pinder brings to the board significant

board experience, including corporate governance expertise. Mr. Pinder

has served on more than 40 public, private, not-for-profit and crown

boards with a focus on the energy sector. Mr. Pinder currently serves

as a director of ARC Resources Ltd. where he is the Chair of the

Policy and Board Governance Committee and is Chair of the board of

directors of Astra Oil Corp. Mr. Pinder also served as a director of

Renegade Petroleum Ltd. from April 2013 to March 2014 during which

time Renegade successfully repelled a leading energy activist fund in

a proxy contest seeking to replace the entire board. -

Thomas A. Budd. Mr. Budd is the President of Focus Advisory

Corp. and an independent businessman. Mr. Budd has extensive

experience providing mergers, acquisitions and financial advice on a

significant number of Canadian oil and gas transactions. Most

recently, Mr. Budd served as President and Vice Chairman, Head of

Investment Banking at GMP Corp. and Griffiths McBurney Canada Corp.

from April 1996 until 2008. Mr. Budd also served as a director of

Renegade Petroleum Ltd. from April 2013 to March 2014 and was the

Chair of Renegade and a member of its special committee during a proxy

contest in which Renegade successfully repelled a leading energy

activist fund seeking to replace the entire board. -

Sandy L. Edmonstone. Mr. Edmonstone is the President of Cation

Capital Inc. Mr. Edmonstone was previously Executive Director and

Deputy Head of Global Oil & Gas within the Macquarie Group, where he

oversaw global energy platform operations. Mr. Edmonstone has advised

on a variety of mergers and acquisitions, asset dispositions,

restructurings and shareholder-value maximization processes. Mr.

Edmonstone has been involved in mandates specifically focused on

securityholder rights, ensuring securityholders receive maximum value

for their investment. Recently, he led an investor initiative that

resulted in approximately 500% additional consideration for

securityholders than what the board had unanimously recommended. Mr.

Edmonstone is also a graduate of the Institute of Corporate Directors’

Education Program, holding the ICD.D designation.

In addition to a wealth of experience comprised of high profile board

work, contested corporate transactions and in-depth public markets

governance experience, Cation’s nominees possess:

-

Enhanced equity ownership through the direct purchase of Crescent

Point shares - Deep knowledge and experience in the energy and commodities business

-

Extensive capital markets expertise required to restore market

confidence and optimize capital deployment - Demonstrated shareholder value maximization experience

Once elected, Cation’s nominees are committed to working with the other

directors to implement a plan to review leadership, restore value and

change the culture at Crescent Point.

The shareholders of Crescent Point should not and cannot continue to

accept these results, especially from a company with such tremendous

assets and potential. Rather, based on study and analysis, we believe

Crescent Point has multiple opportunities to drive significant

shareholder value by:

|

• Fixing misaligned incentives |

|

• Rationalizing capital allocations and high grading the |

|

• Realignment initiatives |

|

• Establishing a business model focused on strong free cash |

Shareholders need new directors with the experience, alignment and

commitment to guide the Company to a new, sustainable, value-creating

strategy

We ask that you vote the BLUE

PROXY or BLUE VIF in

support of our nominees, who are committed to working with the Board and

management to address the Company’s strategy and governance failures and

help it fulfill its potential for all shareholders.

In order to be used at the Meeting, your BLUE

form of proxy or BLUE VIF must be submitted

in accordance with the instructions provided prior to 5:00 p.m. (Calgary

time) on Tuesday, May 1, 2018.

The Time For Change Is Now

Crescent Point’s Underperformance and

Shareholder Value Destruction

Since January 1, 2015, an investment in Crescent Point has generated a

total return of (-55%), significantly below the total returns of the

sector (-19%, TSX Energy Index) and the overall market (+3%, TSX

Composite). During the same period, an index of the Company’s primarily

produced commodity has risen by 18%.

It is clear that the Company’s underperformance cannot be blamed on the

sector or commodity headwinds.

CPG underperformance and shareholder value destruction (See Chart

3)

| Notes: | |

| (1) | Calculations are based on total return as of January 2, 2015. |

| (2) | Source: Bloomberg. |

During this period of shareholder value destruction, the Company has

made repeated changes to its Board, with the board seeing six (with a

seventh nominated this year) new directors cherry-picked by management

over the period beginning in March 2014. Yet, there is no sign that this

has stemmed the decline. If anything, shareholder value destruction has

accelerated. Since 2017, Crescent Point’s share price has declined

50%, versus the sector -17%, the market -1% and WTI +15% and

underperforming by a greater margin than in the prior three years.

Clearly, the current Board has failed shareholders

One key driver of shareholder value destruction has been the Company’s

declining dividend, which has been reduced by 87% over the past four

years. A timely reduction of the dividend that preserved shareholder

value would have been appropriate and prudent (and in line with the

approach adopted by companies in Crescent Point’s peer group). However,

the Company instead elected to delay the dividend reductions relative to

its peers, adopting a “too little, too late” approach that both deprived

the Company of necessary cash on hand and eroded shareholder value.

CPG Historical Dividend (See Chart 4)

| Note: | |

| (1) | Source: Company website; press releases. |

Crescent Point suffers from a significantly discounted valuation, both

relative to its peers and relative to the valuation premium it once

enjoyed. Relative to its peers, Crescent Point has the lowest financial

valuation metrics despite its assets having the highest exposure to

light oil. In order to compete with its peers, it must generate greater

returns on capital.

CPG discounted valuation relative to peers (See Chart 5)

| Notes: | |

| (1) |

Entity Value (“EV”) = Market Capitalization (basic shares outstanding x share price) + Net Debt (working capital deficiency (surplus) + long-term debt). |

| (2) |

Earnings Before Interest Taxes Depreciation and Amortization (“EBITDA”). |

| (3) |

2018E based on consensus estimates (Source: Capital IQ and Bloomberg). P/Cash flow = share price over cash flow for the noted period. |

| (4) |

Based on 2017 year end statements of reserves data and other oil and gas information. PDP = Proved Developed Producing Reserves, Proved = Proved Reserves and P+P = Proved Plus Probable Reserves. |

| (5) |

Based on 2017 year end financial statements. CF = Cash Flow and 18E based on consensus estimates (Source: Capital IQ and Bloomberg). |

| (6) |

Encana values have been converted from $US using the applicable exchange rate as of April 6, 2018. |

Crescent Point’s shareholders cannot continue to endure further value

destruction under the current Board.

A Failure of Strategy and Governance

Despite having a number of years to improve the business, the Company

continues to be plagued with deteriorating performance. Total capital

expenditures for 2017 well exceeded the Company’s original guidance

while actual average annual production increased only slightly and exit

guidance remained flat. All-in general and administrative costs

including capitalized and share-based compensation costs are among the

highest in the Company’s peer group. Proven plus probable finding and

development costs including changes in future development capital have

gone from $7.02/barrel of oil equivalent (“boe”) in 2016 to $21.64/boe

in 2017, and operating costs have increased year over year. The

Company’s key performance indicators are overwhelmingly negative and

continue to deteriorate.

While the current Board may point to the Company’s advertised per share

growth measures, it appears that such calculations ignore the impact of

debt on a per share basis.

The reality is Crescent Point has ignored the impact of its billions of

dollars of debt in calculating its per share growth and, if it were to

account for such debt, per share growth would be negative. The Board’s

focus on growth has come at the cost of operating efficiencies of the

business and material share price erosion.

Impact of debt on a per share basis (See Chart 6)

| Notes: | |

| (1) |

Compound annual growth rate (“CAGR”) calculated by taking the ending value and dividing its value at the beginning of that period, raise the result to the power of one divided by the period length, and subtract one from the subsequent result. |

| (2) |

Reserves are based on the Company’s statements of reserves data and other oil and gas information and other information for the noted periods. Production figures are based on the Company’s reported production as of the year end for the noted periods. Number of issued and outstanding shares is based on the Company’s reported figures as of December 31 for the noted periods. |

| (3) | Based on year end Net Debt for the noted periods. |

| (4) |

Debt-adjusted calculation holds debt constant at 1.5x debt/cash flow. Equity is issued if the ratio is above 1.5x and purchased if the ratio falls below 1.5x. |

The Board and management’s strategy has been to spend capital to grow

production without regard for shareholder return or debt, which has

ballooned. This is demonstrated by higher debt/cash flow leverage than

would have been historically acceptable to the Board.

Notwithstanding poor corporate performance over recent years, remarkably

executive compensation has spiked, with an increase of 17% in total

compensation for 2017 year over year. This has occurred while

shareholders have suffered a ~48% plunge in the value of their shares

over the same period. To add insult to injury, shareholders have

repeatedly demonstrated their dissatisfaction with matters related to

executive compensation without seeing any results, including in the 2016

proxy cycle where Crescent Point received a “no” vote on its say on pay

resolution with a dismal 31% of votes cast in support of the Company's

approach to executive compensation.

Disconnect between executive compensation and shareholder returns

(See Chart 7)

| Notes: | |

| (1) | Figures presented in millions. |

| (2) |

Source: Company information circulars – proxy statements for the noted periods and Bloomberg. |

This complete disconnect between executive compensation and shareholder

returns is deeply troubling and further illustrated by the fact that the

Company’s current directors and officers own just 0.6% of the issued and

outstanding shares. In contrast, our nominees own an aggregate of 0.3%

of the issued and outstanding shares, which is more than double the

amount of shares held by all of the incumbent non-employee directors.

Yet it would seem the Company intends to go a step further and actually

reward management for destroying shareholder value. With the Company’s

shares hovering, over the course of the last year, near a 15-year low,

we shareholders would expect a Board and management team whose interests

are aligned with shareholders to be buying shares. Instead, at the

upcoming annual general meeting, the Company is seeking to further

enrich its executive leadership team by adopting a new equity

compensation plan and ratifying grants of nearly 3 million options made

without shareholder approval but with apparent urgency, when the shares

were reaching lows earlier this year. With a correspondingly depressed

exercise price, these options are essentially risk-free money – for

management, at shareholders’ expense – that rewards insiders for having

decimated the share price.

As if that weren’t enough, the Company is also asking shareholders to

approve an increase in the number of shares eligible for issuance under

the Company’s existing restricted share bonus plan. It is outrageous to

so richly reward a leadership team that has presided over the

evisceration of shareholder value that has befallen Crescent Point.

Crescent Point’s current strategy and governance structures, as

overseen by the current Board, are failing the Company and its

shareholders

STRATEGY FOR VALUE CREATION

We believe the opportunity at Crescent Point is unique, both in the

amount of value that can be unlocked and how readily it can be achieved.

Cation believes a new strategy needs to be implemented at Crescent Point

to create shareholder value over the next 18 months, focused on

maximizing shareholder value through both near and long-term initiatives

for which the proposed Board members would seek to build consensus with

the remaining Board members and management.

|

1. Elect Highly Qualified and Fully Independent New |

|

|

2. Undertake a Fulsome Value Maximization Strategy |

The reconstituted Board would undertake a 12 to 18 month fulsome evaluation of the Company’s entire operations, governance and management with a view to identifying near-term opportunities for gain while ensuring the long-term sustainability of the business |

|

3. Realign the Business |

Our nominees are intent on realizing immediate value for all stakeholders and eradicating the bureaucratic bloat and inefficiencies currently plaguing Crescent Point. Specific measures that may be pursued include:

Key to the realignment effort will be our focus on identifying |

|

4. Redeploy the Efficiencies and Synergies into Ensuring |

Once the Company realizes the benefit of enhanced cash flows from its realignment initiatives and reduced cost of capital, it will be able to reward shareholders through any, all or a combination of:

|

|

5. Dividend |

Initially maintain the existing dividend and review the dividend policy regularly based on the value maximization and realignment efforts outlined above and the cash flow performance of the Company |

Contacts

Investors:

D.F. King & Co

1-800-835-0437 toll-free

in North America

1-201-806-7301 outside of North America (collect

calls accepted).

or

Media:

Gagnier Communications

Dan

Gagnier / Jeffrey Mathews / Patrick Reynolds

1-646-569-5897